YTL SGREIT's 1Q FY15/16 NPI increase by 10.2% on contributions from new acquisition and Singapore portfolio

SINGAPORE, 27 October 2015

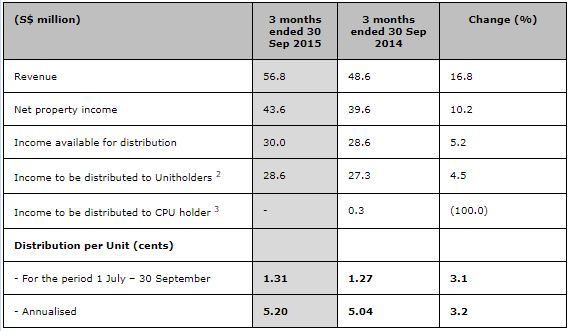

YTL Starhill Global REIT Management Limited, the manager of SGREIT, is pleased to announce the results for the three months ended 30 September 2015 (1Q FY15/16). Revenue for SGREIT group grew 16.8% over the previous corresponding period to S$56.8 million in 1Q FY15/16 and net property income (“NPI”) for 1Q FY15/16 grew 10.2% over the previous corresponding period to S$43.6 million. The growth in revenue and NPI was mainly driven by the fullquarter contribution from the recently-acquired Myer Centre Adelaide and Singapore portfolio performance, partially offset by lower contributions from China and net foreign currency movements. Income to be distributed to Unitholders was S$28.6 million for 1Q FY15/16, 4.5% higher than that of S$27.3 million for the previous corresponding period of three months ended 30 September 2014.

Distribution Per Unit (“DPU”) for the period from 1 July 2015 to 30 September 2015 was 1.31 cents, 3.1% higher compared to the 1.27 cents achieved for the previous corresponding period. On an annualised basis, the latest distribution represents a yield of 6.89% [1] . Unitholders can expect to receive their 1Q FY15/16 DPU on 27 November 2015. Book closure date is on 4 November 2015 at 5.00 pm.

Overview of Starhill Global REIT’s financial results

Tan Sri Dato’ (Dr) Francis Yeoh, Executive Chairman of YTL Starhill Global, said, “Asia’s growth will moderate slightly on the back of risks from China’s economic rebalancing and the pace of expected normalisation of US policy interest rates. Notwithstanding the uncertain macroeconomic outlook, we will continue to maintain a strong financial standing which should enable us to tap on any opportunities that might arise.”

Mr Ho Sing, CEO of YTL Starhill Global, said, “We started the new financial year with a robust performance in the first quarter. Led by the sustained strength of our Singapore portfolio and the fullquarter contribution from our recent acquisition of Myer Centre Adelaide, NPI grew by 10.2% y-o-y in 1Q FY15/16. Our master/long-term leases, with the inclusion of Myer’s long-term lease, provide income stability for the Group. We have no significant debt refinancing requirement until 2018 and all our borrowings remain fully hedged via a combination of fixed rate debt and interest rate caps and swaps.”

Review of portfolio performance

SGREIT’s Singapore portfolio, comprising interests in Wisma Atria and Ngee Ann City on Orchard Road, contributed 60.1% of total revenue, or S$34.1 million in 1Q FY15/16. NPI for 1Q FY15/16 increased by 3.6% y-o-y to S$26.9 million, led by positive rental reversions achieved in previous quarters, partially offset by higher operating expenses. Singapore retail portfolio recorded negative rental reversions of 7.3% for leases committed in 1Q FY15/16 to accommodate new retail concepts. The leases committed for the quarter accounted for less than 3% of Singapore retail portfolio’s revenue excluding Toshin master lease at Ngee Ann City Retail. Wisma Atria Retail revenue increased 7.7% y-o-y and its NPI grew 5.6% over the previous corresponding period on the back of higher revenue. Tenant sales at Wisma Atria rose 1.1% y-o-y in 1Q FY15/16 mainly due to contributions from tenants which have recently started their operations at the mall. However, shopper traffic was down 9.7% y-o-y as the strata area owned by Isetan remained closed for its renovations.

Isetan’s new tenant in the basement level, Mango, has since commenced operations in September 2015. Revenue from Ngee Ann City Retail gained 0.9% y-o-y while NPI increased 1.0% y-o-y. The Singapore office portfolio continued to benefit from healthy leasing demand amidst limited upcoming office supply space in Orchard Road as revenue and NPI increased 4.3% and 4.1% respectively in 1Q FY15/16 over the previous corresponding period, on the back of 3.5% positive rental reversions for leases committed in 1Q FY15/16. As at 30 September 2015, approximately one-third of the office leases due for expiry in FY15/16 by gross rent have been committed (renewed & new leases).

SGREIT’s Australia portfolio, comprising Myer Centre Adelaide in Adelaide, South Australia, and the David Jones Building and adjoining Plaza Arcade in Perth, Western Australia, contributed 23.0% of total revenue, or S$13.1 million in 1Q FY15/16. NPI for 1Q FY15/16 was S$8.6 million, 113.2% higher than the previous corresponding period mainly due to the full-quarter contribution from the recentlyacquired Myer Centre Adelaide, partially offset by depreciation of the Australian dollar against the Singapore dollar and lower occupancies at David Jones Building. For the asset redevelopment plans at Plaza Arcade to accommodate anchor tenants and optimise upper-storey space, we are in negotiations with prospective anchor tenants.

SGREIT’s Malaysia portfolio, comprising Starhill Gallery and interest in Lot 10 along Bukit Bintang in Kuala Lumpur, contributed 11.5% of total revenue, or S$6.5 million in 1Q FY15/16. NPI for 1Q FY15/16 was approximately S$6.3 million, 16.0% lower than the previous corresponding period, mainly due to depreciation of the Malaysian ringgit against the Singapore dollar and reversal of excess provision of property taxes in the previous corresponding period following the revision in property tax assessment. More than 70% of our net foreign income in Malaysian ringgit for 1Q FY15/16 was hedged via foreign exchange forward contracts.

Renhe Spring Zongbei in Chengdu, China, contributed 3.4% of total revenue, or S$1.9 million in 1Q FY15/16. NPI for 1Q FY15/16 was S$0.9 million, a decline of 27.5% from the previous corresponding period. The decline was largely attributed to lower revenue as the high-end luxury retail segment continues to be impacted by the austerity measures the central government has put in place, as well as increasing challenges and competition from new and upcoming malls in the city.

In 1Q FY15/16, SGREIT’s Japan portfolio, which comprises five properties located in central Tokyo, contributed 2.0% of total revenue. NPI for 1Q FY15/16 was S$0.9 million, 11.5% higher than in the previous corresponding period, largely attributable to higher occupancies and lower operating expenses, partially offset by depreciation of the Japanese yen against the Singapore dollar. The overall committed portfolio occupancy improved to 98.1% as at 30 September 2015 with full occupancies maintained in four out of its five properties.

Back